This story is the first in a four-part Grist series examining how climate transpiration is destabilizing the global insurance market. It is published in partnership with the Economic Hardship Reporting Project.

“We’ve got ourselves a little monster out there,” reporter Jim Cantore warned, facing the camera in the Weather Channel’s newsroom on a sultry August weekend in 1992. At first, few in Florida were paying attention. “It’s very nonflexible to get people to believe that there’s some danger from some element of nature that they haven’t experienced before,” a reporter told Cantore, as the waterworks played tape of tranquil beaches and neat vacation homes.

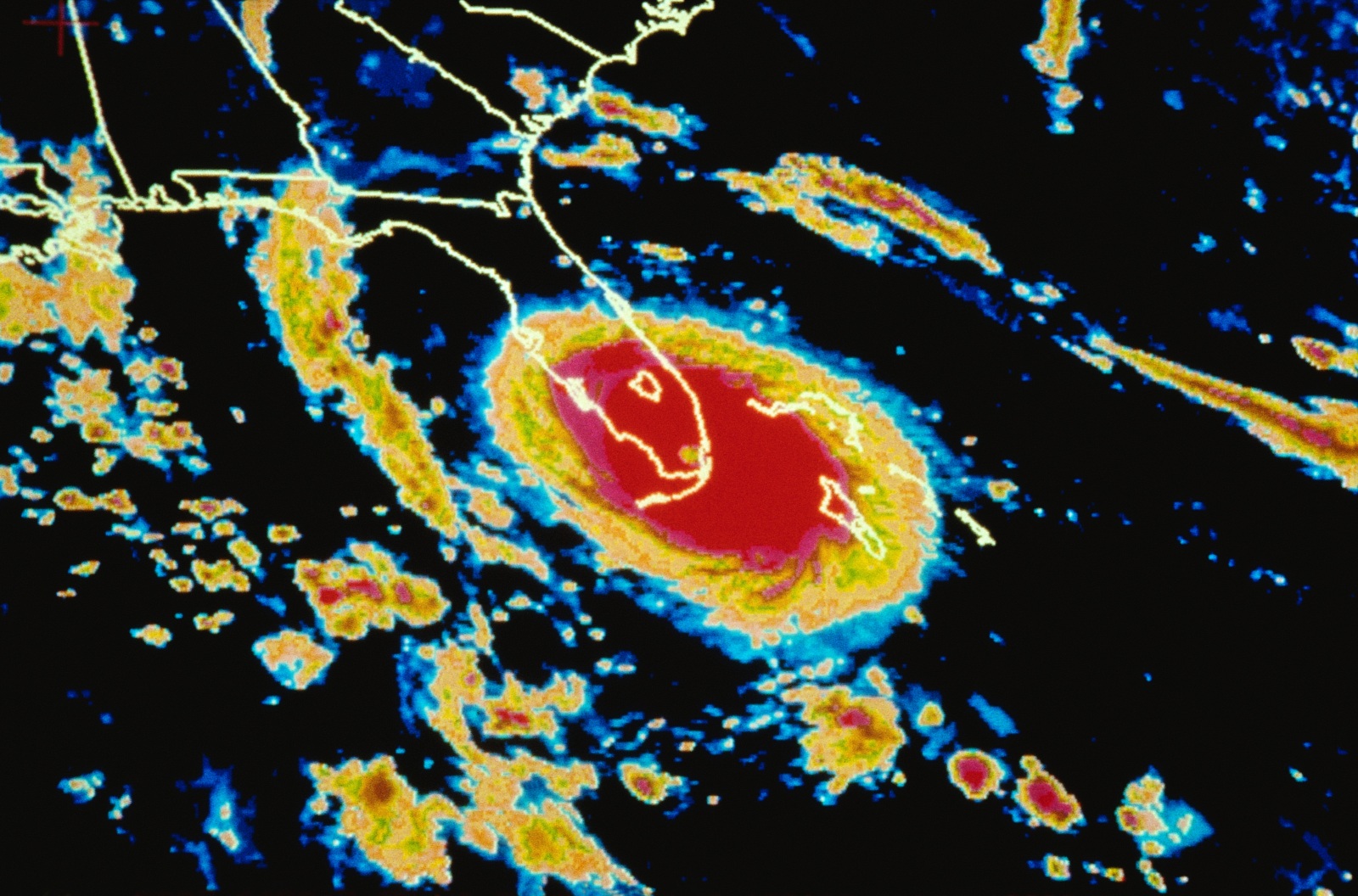

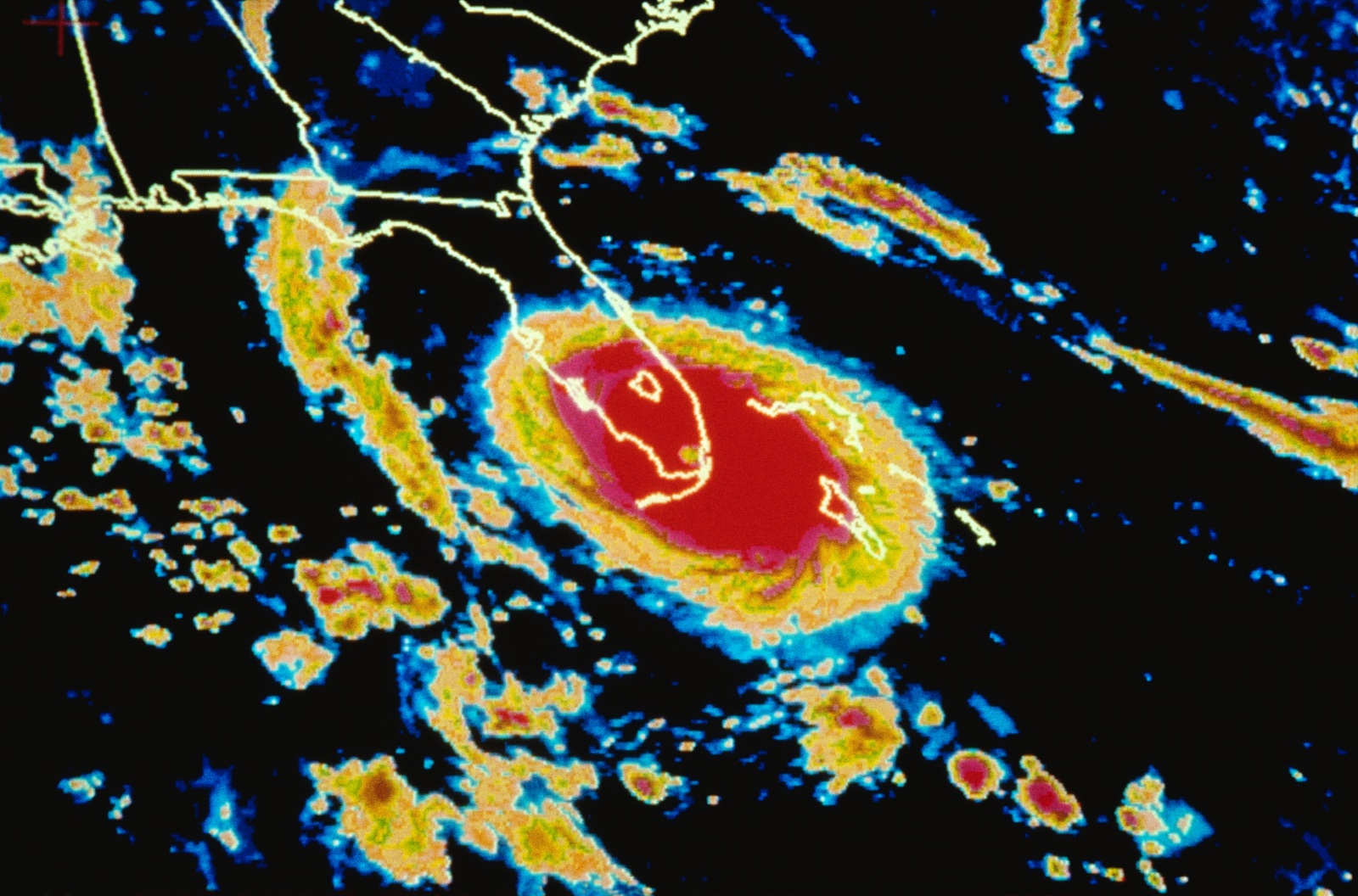

As the storm approached Florida, it gained the moniker Andrew, rapidly intensifying into a Category 5 hurricane as it exceeded wind speeds of 165 mph. Karen Clark watched updates on TV from her home in Boston with fascinated horror — and her career on the line.

Most insurance companies at that time assessed hurricane exposure in their portfolios by simply multiplying consumer premiums by a rough factor of supposed risk, rather than tracking very property replacement costs. “They were just very transplanted formulas,” she said.

So in 1987, Clark had started her own company, Applied Insurance Research, or AIR, to develop software that largest unscientific the potential losses from catastrophic events. Unlike the rest of the industry, she used granular data and sophisticated analyses, an tideway now tabbed ending modeling. Her first computer model unscientific that a Category 5 hurricane hitting Dade County could rationalization losses scrutinizingly 10 times increasingly than previously believed. She warned her customers well-nigh the risk in Florida, but until Hurricane Andrew, no one listened. “The good ol’ boys at Lloyds [of London], you know, they thought they had it all figured out,” she said. “They didn’t need any help from this American woman delivering virtually a little computer.”

By that Sunday morning in 1992, it became well-spoken that Andrew’s eye was aiming straight for Miami. Clark rushed into the AIR office, where her models suggested that the storm could rationalization at least $13 billion in damages — a disaster so expensive at first she debated whether she should publish the results.

As the hurricane made landfall the next day, it tore palm trees from the ground and stripped roofs from houses, scarification a devastating path wideness southern Florida. Over 100,000 homes were damaged, and an spare 50,000 were destroyed. When a vendee tabbed asking well-nigh his probable losses, Clark told him virtually $200 million dollars. “He said, ‘For the industry?’ and I was like, ‘No. For your company.’” AIR’s estimates turned out to be conservative: Andrew sooner forfeit the insurance industry $15 billion.

In the aftermath, Clark said, “everyone knew the market was going to radically change.” The ending models she ripened quickly became the industry standard, waffly how American companies navigated risk from natural disasters.

In hindsight, it was the whence of the dynamic now driving insurance markets. To handle massive payout events like Andrew, insurance companies sell policies wideness variegated markets — historically, a hurricane wasn’t hitting Florida in the same month a wildfire wiped out a town in California. They themselves moreover pay for insurance, a financial instrument tabbed reinsurance that helps distribute risk wideness geographic regions. Reinsurance availability remains a major suburbanite of what insurance you can buy — and how much it costs.

But as climate transpiration intensifies lattermost weather and claims pile up, this system has been thrown into disarray. Insured losses from natural disasters in the U.S. now routinely tideway $100 billion a year, compared to $4.6 billion in 2000. As a result, the stereotype homeowner has seen their premiums spike 21 percent since 2015. Perhaps unsurprisingly, the states most likely to have disasters — like Texas and Florida — have some of the most expensive insurance rates. That ways overly increasingly people are forgoing coverage, leaving them vulnerable and driving prices plane higher as the number of people paying premiums and sharing risk shrinks.

This vicious trundling moreover increases reinsurers’ rates. Reinsurers globally raised prices for property insurers by 37 percent in 2023, contributing to insurance companies pulling when from risky states like California and Florida. “As events are getting worthier and increasingly costly, that has raised the prices of reinsurance in those areas,” said Carolyn Kousky, the socialize vice president for economics and policy at the Environmental Defense Fund, who studies insurance. “It’s tabbed the hardening of the market.”

In a worse-case scenario, this all leads to a massive stranded windfall problem: Premiums get so upper that property values plummet, families’ investments dissipate, and banks are stuck holding what’s left.

More simply, the global process for handling life’s risks is breaking down, leaving those who can least sire it unprotected.

The idea of distributing risk has been virtually since the 14th century, when insurers of trading ships wanted someone to share the uncertainties of long sea voyages. Modern reinsurance was established in 19th century Europe, which some historians credit to large fires in Hamburg, Germany, and Glarus, Switzerland, where significant losses led to the founding of many of today’s leading reinsurance companies.

These companies were moreover some of the first to issue warnings well-nigh climate change. When in 1973, Munich Re, one of the world’s major reinsurance firms, noticed a spike in the number of inflowing forfeiture claims. In a prescient report, the visitor noted “the rising temperature of the Earth’s atmosphere,” due to the “rise of the CO2 content of the air, causing a transpiration in the traction of solar energy.”

Now, the world is reaping the consequences of that change. In the last decade, the frequency of global natural catastrophes jumped by 28 percent. On a single day in July, 60 percent of the U.S. population faced an lattermost weather alert. Financing have catapulted too: Since 1970, losses from disasters increased an stereotype 5 percent a year, particularly in the United States. That’s considering forfeiture moreover depends on vulnerability and exposure — where people live, and how prepared they are. Tragically, the fastest-growing counties moreover squatter some of the highest risks. “It doesn’t have to be one of these huge events,” said Alice Hill, senior fellow at the Council on Foreign Relations who studies climate consequences. “It’s [also] successive events, back-to-back,” like the 12 atmospheric rivers that hit California this winter.

Reinsurers are particularly exposed to these hazards considering many insurance companies seek primarily to imbricate catastrophic risks — major events like hurricanes that are intensifying as the world warms. In a letter to shareholders this summer, Christian Mumenthaler, the group CEO of global reinsurance visitor Swiss Re, wrote, “Climate transpiration continues to take its toll … wideness multiple geographies.”

As a result, the reinsurance industry has paid dearly for much of the last decade; underwriting losses crush $115 billion in global reinsurance losses in 2022. “There’s a tension over a merchantry model that’s retrospective, with a risk that’s emerging,” said Frank Nutter, president of the Reinsurance Association of America. The financial foundation of insurance, in other words, is cracking.

“Without global reinsurance, we wouldn’t have the topics to provide sufficient disaster coverage for everyone,” Kousky said. “It’s essential.” But unlike insurers, who squatter political pressures from state regulators to alimony rates affordable, reinsurance is much increasingly of a self-ruling market. A recent report from Moody’s finds that reinsurers are reacting by raising their rates, limiting their coverage, and plane deciding to reduce their exposure in places like Florida. Increasingly, the reinsurance industry is reassessing what are known as “secondary perils,” or things like flooding and wildfires — hazards that were previously less plush than major events like hurricanes, but which are rhadamanthine increasingly common.

Because getting risk wrong is now so costly, there’s been a race in the private sector to model future odds. Jenny Dissen works at the North Carolina Institute for Climate Studies, a research institute that’s part of NOAA’s Cooperative Institute for Satellite Earth System Studies. She says she commonly fields calls from insurers eager to know the latest climate indicators. Yet critics worry this rush to fine-tune risk predictions may potentially slide skyrocketing premiums. Since many are proprietary, the accuracy of these assessments can be difficult to vet. They are moreover having unintended consequences, like lowering municipal bond ratings, hindering governments’ worthiness to respond to lattermost weather by raising funds.

Some believe that an individual focus is likely not the weightier — or most equitable — way to write climate adaptation. “Many of these version steps are like a kind of public good,” that can’t be taken on an individual level, like towers a seawall, said Madison Condon, Boston University law professor and corporate and environmental law professor. “They work weightier if everyone takes them.”

The economic implications of all this are troubling. A new report by the U.S. Treasury Department, released at the end of June, found major gaps in the supervision and regulation of insurers. The report well-considered much closer sustentation to “the risks the insurance industry may pose to the overall financial sector.”

While insurance prices have soared, a recent report from the nonprofit First Street Foundation estimates that 39 million homes are covered at prices artificially lower than their true risk. The authors suggest that state regulations capping premiums and government-backed insurer-of-last-resort programs have unseen the extent of the crisis. They predict that as disasters protract surging, what they undeniability the “growing climate rainbow in the housing market” will pop — leaving millions of homes uninsurable and destroying their value. The stereotype homeowner who loses an insurance policy automatically sees a waif of increasingly than 10 percent in the home’s value, the report notes. “If the value of their home plummets or if the credit agencies downgrade their communities,” Hill said, “one of my big fears is we’re going to have a lot of people trapped in places that are unsafe, economically trapped.”

Such concerns prompted the Treasury Department last year to require 213 large insurers — companies like Allstate and Farmers Insurance — to provide data well-nigh their homeowner policies. Its initial goal was to collect information well-nigh coverage, claims, and premiums by zip lawmaking to identify where climate transpiration may disrupt markets. The plan faced fierce opposition from the industry, which says it’s a regulatory undersong and that disclosing this data may harm companies’ competitive advantage. Results are not predictable in 2023, and will not include other worldwide types of insurance impacted by climate, like inflowing insurance — which is often covered in a separate policy from homeowners insurance.

This spring, one of the largest insurance brokerage companies warned Congress they weren’t moving fast enough. “Just as the U.S. economy was overexposed to mortgage risk in 2008, the economy today is over-exposed to climate risk,” Aon PLC president Eric Anderson told Senate upkeep committee members. Yet there appears to be little federal urgency in addressing the problem.

Experts warn that increasing prices may tip homeowners toward default as increasingly insurers flee. At least five major companies have stopped writing coverage in some regions. State Farm announced this spring that it would stop selling homeowners’ policies in California. The visitor cited “rapidly growing ending exposure, and a challenging reinsurance market.” Allstate moreover quietly stopped writing new policies in the Golden State in June. In Louisiana, where at least 20 companies have left in the last two years, the situation has gotten so bad the state passed a $45 million funding bill in 2023 in an effort to woo insurers back.

Though government has been slow to write these trends, global financial markets are once basing investment decisions on climate risks. Major ratings companies like Moody’s and McKinsey have recently purchased climate data firms. First Street Foundation, for example, provides climate risk information to many banks, major reinsurers, and government agencies — including Fannie Mae and Freddie Mac, which are once using it to screen for mortgages’ climate exposures. Mortgage-purchasers like these, without all, are the ones who may soon be left holding the carrion of assets.

Meanwhile homeowners, many of whose mortgages require insurance, are left with limited options. Without six property insurance companies in Florida supposed bankruptcy in 2022, for instance, many property owners had to turn to state-run insurers, like Florida’s Citizens Property Insurance Corp., a government-backed entity serving otherwise uninsurable populations. Although its policies tend to be less comprehensive than private insurance, in the last year, its ranks swelled well-nigh 50 percent, to virtually 1.7 million people. Yet this year, as Florida’s reinsurance rates skyrocketed 30 to 50 percent, plane these last-resort policy rates spiked 12 percent, leaving many families to weigh whether they can sire to alimony their insurance.

If the state is hit by a major hurricane, the program has grown so large the resulting claims could outstrip Citizens’ budget. The program can’t go out of merchantry like a private company, but if it runs out of money, Florida law allows Citizens to issue one-time bills charging customers up to 45 percent of their yearly premium. Someone who just lost their home in a hurricane, in other words, could be facing a surprise snout of thousands of dollars.

Not only is that bad for the families whose losses aren’t protected, it deepens existing inequities. Right now, the insurance market is unintentionally protecting wealthy property owners while socializing their risk through highly subsidized premiums. The federal government holds the liability for the majority of inflowing insurance, for example, managed by the Federal Emergency Management Agency. Repeatedly flooded properties make up just 1 percent of the program’s policies but account for increasingly than 30 percent of the claims. “When the government’s the replacement insurer, the taxpayers have to support that,” Hill said.

Two out of every three American homes are now underinsured, meaning owners may squatter major financial losses if they were to endure a disaster. The effects won’t be felt equally. There can be an inherent tension between climate-related financial risks and anti-redlining efforts: People of verisimilitude who have long suffered favoritism are now disproportionately living in areas at greater danger of disaster. That makes it difficult to both price climate risks and not divest from underserved communities.

Despite stuff one of the first to understand these perils, insurers protract to contribute to them. They’ve played a major role in emissions for decades: Without insurance, fossil fuel companies have difficulty obtaining financing. Coal is an apt example of what happens when insurers withdraw from a market — since 45 insurers are phasing out of coal policies, construction of new coal-fired power declined by 84 percent between 2015 and 2018.

But insurers have been slower to move yonder from oil and gas, in part considering it’s a larger part of many companies’ business. In June, the Senate Upkeep Committee sent letters to major insurance companies asking for information well-nigh how much each visitor earns from the fossil fuel industry. “[I]t is difficult to understand how the industry can thoughtfully price and manage climate risk in some areas of its business,” committee members wrote, “while simultaneously having no unveiled plan to phase out its underwriting of and investment in the projects and companies generating the emissions that are causing these very harms.”

Prompted in part by concerns over this kind of liability, the reinsurance industry has begun warning well-nigh the need to reduce climate risk. “The economic and insured losses over time are a well-spoken indicator that the past is not a representation of the future,” said Raghuveer Vinukollu, throne of climate insights at Munich Re US. Physical mitigation, like towers inflowing walls and buffer zones will be needed, he says, but funding and towers these engineering measures can be difficult.

With insurers themselves running out of insurance options, the stability of financial systems is far shakier than many realize. Yet the federal government hasn’t ripened a national version plan that comprehensively addresses these concerns. In its absence, decisions are left to municipal and state governments, some of which are facing serious blowback. When Hawai‘i recently attempted to increase setbacks for future oceanfront construction, for example, citing firsthand sea-level rise, homeowners managed to stall the plan. Experts like Condon undeniability for a internal national climate service that can help guide these adaptations and regulatory policies, based on transparent and specific risk assessments.

“If you want to know the truth, the science is the easy part,” Karen Clark said. Getting people to transpiration their behavior, on the other hand, is difficult. She is still working on catastrophic modeling, now at her eponymous firm, where she urges decisionmakers to get increasingly realistic, and quickly. “People don’t understand a vital economic law — there’s no self-ruling lunch. There’s a risk,” she said. “Somebody’s paying for it. It’s just a question of who.”

This story was originally published by Grist with the headline As climate risks mount, the insurance safety net is collapsing on Oct 10, 2023.